Posts

For decades analysts and policymakers have tried to understand mortgage performance by staring at national aggregates – national home price indices, national unemployment rates. national delinquency curves. These measures are tidy and convenient, but they tell us remarkably little about the forces that actually push a household into default. National models cannot succeed, because mortgage…

Read More

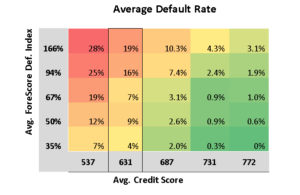

Every mortgage investor faces the same question: Two borrowers have identical credit scores. Which loan is safer? Answering that question well means looking at ForeScore, credit score, and mortgage risk together, rather than treating credit history as the whole story Conventional mortgage valuation has no satisfactory answer. A credit score summarizes a borrower’s financial history,…

Read More

Mortgage underwriting has long focused on the individual borrower. Credit scores, loan-to-value ratios, debt-to-income ratios, income stability, and documentation quality remain the foundation of modern credit analysis—and for good reason. These variables capture a borrower’s capacity and willingness to repay. Yet they tell only part of the story. A mortgage is secured by a property embedded…

Read More

One of the central promises of modern finance is that risk can be reduced by sharing it. If thousands of mortgages are pooled together and sold to investors around the world, the default of any one borrower should matter very little. Mortgage securitization failed in the 2008 financial crisis. Wall Street did not see this coming ….…

Read More

Mortgage default is often described as a financial decision—an optimization problem where borrowers weigh the costs and benefits of continuing to pay. Capozza et al. remind us that this framing is incomplete. Default is also a household economic shock story, and those shocks are overwhelmingly local — local economic shocks trigger mortgage default. Borrowers don’t…

Read More

In the world of economics, we don’t look for villains; we look for incentives. If you read UFA’s (ACV, 2011) autopsy of the mortgage meltdown, you see a story not just of greed, but of a massive failure in the structural mechanics of our cities and our credit markets. Let’s revisit the 2008 housing crisis…

Read More

Earlier (“Why Mortgage Risk is Local; not National”) we established that mortgage default is fundamentally a local process, This blog explains why: because the most powerful driver of borrower behavior—the home equity position—is itself a product of local price cycles, not national averages. Local home price cycles drive mortgage default rates. Capozza and co-authors highlight…

Read More

What caused the 2008 financial crisis? Most explanations fall into familiar categories: reckless lenders, irresponsible borrowers, or a housing bubble that simply grew too large. These narratives contain pieces of the truth, but they miss the deeper structural forces that made the system fragile long before the first mortgage default. Rethinking the Story UFA’s framework…

Read More

Housing markets have always been shaped by geography, but in today’s economy the divergence across American metros has become impossible to ignore. Some regions—Texas and Florida among them—are experiencing sharp corrections, while others continue their long ascent. These patterns are not random noise; they reflect the deep and durable forces that shape cities, migration, and…

Read MoreIn the world of mortgage investing and credit risk modeling, subprime borrowers—those with credit scores between 550 and 650—present a unique and complex risk profile. While these loans can be priced profitably, they require a fundamentally different approach than prime credits. Here’s why. 🔍 Subprime vs. Prime: Behavioral Divergence Subprime credits don’t just carry more…

Read More