A Nation of Many Housing Markets: Rising Default Risk Amid Sharp Regional Divergence

Spring 2026

The UFA National Default Risk Index (NDRI) ticked up sharply in the second quarter of 2026, rising to 131, a twelve point increase from the revised first quarter reading of 119. In practical terms, today’s economic climate implies that a newly originated mortgage carries a 31 percent higher probability of default than an equivalent loan made in the 1990s—an estimate derived solely from shifts in local and national economic fundamentals. That is the central finding of the latest analysis from University Financial Associates of Ann Arbor.

While an index level of 131 remains far below the Great Financial Crisis (GFC) peaks above 200, national aggregates can be deceptive. Housing markets are not a single organism but a patchwork of local ecologies, each responding to its own supply constraints, migration flows, and economic shocks. The national number, in other words, is the average of a boom and a bust.

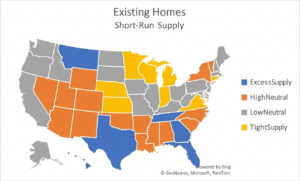

This quarter’s map makes the point vividly. Across the South and Mountain West, inventories of existing homes have climbed above historically neutral levels—a classic early warning sign. Texas and Florida, long magnets for population inflows, now show metros such as Austin and Miami posting meaningful price declines. By contrast, northern markets—especially in the Midwest—continue to exhibit tight supply and rising real prices. Defaults, as always, follow the local cycle, not the national headline.

“Excess supply precedes falling home prices, and falling prices paired with weakening local economies are the textbook precursors to mortgage default,” said Dennis Capozza, Professor Emeritus of Finance at the University of Michigan and a founding principal of UFA. “But the structural tinder that fueled the GFC—thin equity cushions, speculative lending, negative amortization products—is largely absent today. The risk of a repeat remains remote.”

The UFA Default Risk Index measures the risk of default on newly originated mortgages. UFA’s analysis is based on a ‘constant-quality’ loan, that is, a loan with the same borrower, loan and collateral characteristics. The index reflects only the changes in current and expected future economic conditions, which are less favorable currently than in prior years.

Each quarter UFA evaluates economic conditions in the United States and assesses how these conditions will impact expected future defaults, prepayments, loss recoveries and loan values for nonprime loans. A number of factors affect the expected defaults on a constant-quality loan. Most important are worsening economic conditions. A recession causes an erosion of both borrower and collateral performance. Borrowers are more likely to be subjected to a financial shock such as unemployment, and if shocked, will be less able to withstand the shock. Fed easing of interest rates has the opposite effect.

UFA’s pioneering mortgage analysis has successfully predicted problems in the mortgage market well in advance including the increased defaults in Southern California in the mid-90s and the recent national mortgage crisis. Its predictions are based on an extensive analysis of local economic conditions in each state and the relationship of those conditions to loan performance. The historical record of millions of mortgage loans is studied each quarter to assess the vulnerability of each state to loan losses and prepayments. The detailed analysis of each state – including best and worst places to lend – is available in the UFA Mortgage Report, published on a quarterly basis.