Housing markets have always been shaped by geography, but in today’s economy the divergence across American metros has become impossible to ignore. Some regions—Texas and Florida among them—are experiencing sharp corrections, while others continue their long ascent. These patterns are not random noise; they reflect the deep and durable forces that shape cities, migration, and economic opportunity. And as these forces intensify, the traditional tools of credit risk assessment are showing their age.

🌐 Why Location Matters More Than Ever

In this environment, UFA’s ForeScore Data Location Scores represent something rare in finance: a genuinely new source of predictive power, grounded not in borrower psychology but in the structural realities of place.

Across the world, lenders have long understood that geography encodes information about economic resilience. In countries such as India—where credit scores are sparse or inconsistent—location-based metrics are not a luxury but a necessity. What is striking in UFA’s recent analysis is that even in the data-rich U.S. mortgage market, Location Scores rival credit scores in their economic importance and surpass them in statistical precision.

This should not surprise us. Credit scores can be gamed; neighborhoods cannot. Borrowers may rearrange their finances in anticipation of a loan, but they cannot easily alter the labor market, housing supply elasticity, or economic dynamism of the place they live. Location Scores capture these structural forces—forces that urban economists have documented for decades.

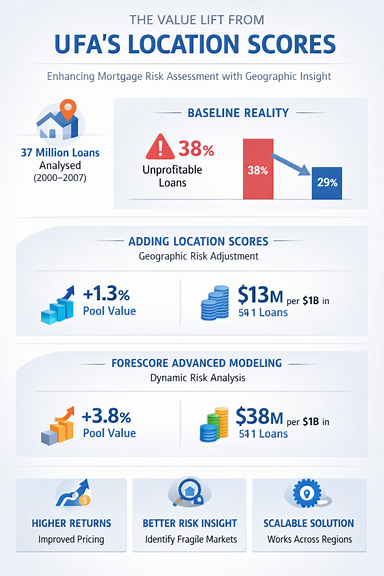

🧪 The Experiment: 37 Million Loans, One Clear Result

UFA examined an extraordinary dataset: 37 million mortgage loans originated between 2000 and 2007. Using standard static default models, most loans appeared sound. Yet a deeper valuation revealed a more sobering truth: 38% of these loans were unprofitable once realistic default risk was accounted for.

Introducing Location Scores required no exotic machinery. Simply multiplying existing default estimates by the indexed Location Score—raising risk in fragile markets, lowering it in resilient ones—was enough to reprice a quarter of the unprofitable loans. The share of unprofitable loans fell from 38% to 29%, and the value of a typical billion‑dollar pool rose by 1.3%, or $13 million.

In a world where basis points matter, this is not a rounding error. It is a material improvement in the accuracy of risk assessment.

🔍 Going Deeper: ForeScore Innovations

Of course, the geography of risk is not static. Markets evolve, and risk evolves with them. UFA’s ForeScore suite incorporates this dynamic reality by adjusting for market risk and modeling future defaults using competing hazards methods. These tools acknowledge a fundamental truth: riskier loans carry more systematic exposure and should be discounted accordingly.

When these innovations are fully applied, the results are even more striking:

- 38% of loans are repriced

- Pool value increases by 3.8%, or $38 million per $1 billion

This is the kind of improvement that comes not from tinkering at the margins but from understanding the underlying mechanics of the system.

🧠 The Takeaway

Credit scores transformed lending decades ago by quantifying borrower behavior. Location Scores represent the next leap, quantifying the structural forces of place with greater precision and far less susceptibility to manipulation. They are especially valuable in markets where credit data is thin, but even in the U.S. they provide a stabilizing lens through which to view increasingly volatile housing dynamics.

As mortgage markets fragment and regional fortunes diverge, lenders need tools that reflect the real geography of risk. UFA’s Location Scores offer exactly that: a scalable, empirically grounded framework for smarter, more resilient lending decisions.