One of the central promises of modern finance is that risk can be reduced by sharing it. If thousands of mortgages are pooled together and sold to investors around the world, the default of any one borrower should matter very little. Mortgage securitization failed in the 2008 financial crisis. Wall Street did not see this coming …. Diversification, after all, is one of the oldest ideas in finance.

Yet in 2008, this logic appeared to fail spectacularly. Securities that had received the highest credit ratings lost enormous value, financial institutions across the globe suffered massive losses, and a downturn in the U.S. housing market became a worldwide financial crisis.

Why?

The conventional answer points to reckless lending, excessive leverage, or failures of regulation. Each played a role. But Anderson, Capozza, and Van Order (2011) identify a more fundamental problem. Securitization did not create a safer financial system because it was built on mortgages that were themselves increasingly fragile. Instead of diversifying risk, it spread the same vulnerability throughout the global financial system.

The Promise of Securitization

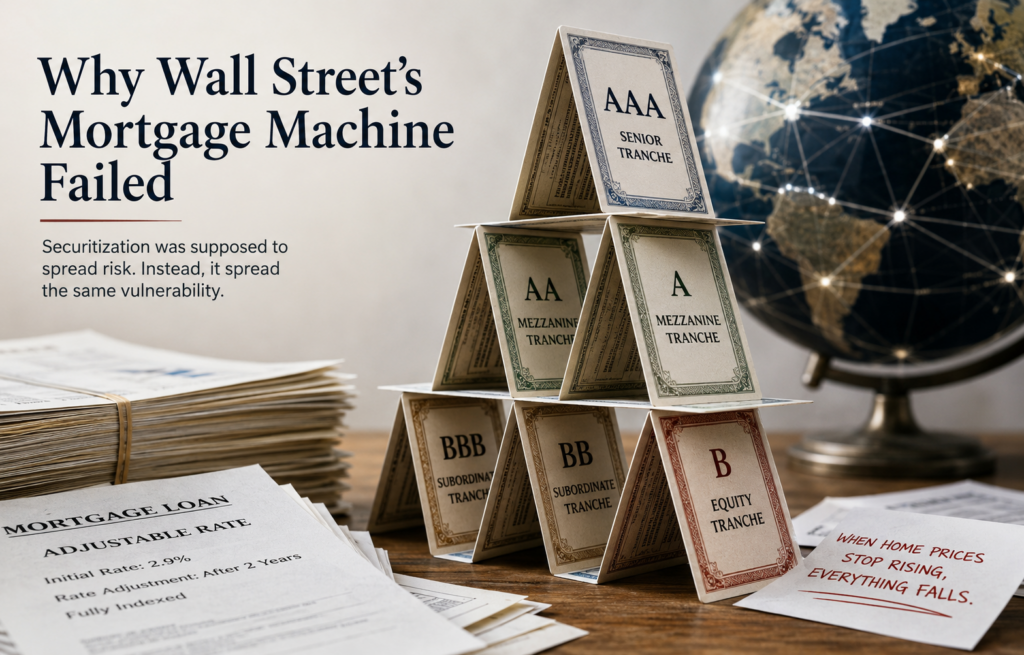

At its core, securitization is a simple and valuable innovation. Mortgage payments from thousands of homeowners are pooled together and divided into securities with different levels of risk. Conservative investors purchase the safest claims, while others accept greater risk in exchange for higher returns.

This structure works remarkably well—provided the underlying mortgages are reasonably independent of one another. If one homeowner loses a job or encounters financial hardship, the losses are absorbed by the large pool. Diversification does what it is supposed to do.

The difficulty is that diversification protects against independent risks. It offers far less protection when many borrowers fail for the same reason at the same time.

A System Built on One Assumption

During the housing boom, mortgage lending increasingly relied on products that depended on continuous refinancing rather than gradual repayment. As discussed in a previous post, many borrowers could afford their mortgages only if rising home prices allowed them to refinance before monthly payments increased.

This changed the nature of mortgage risk.

Instead of thousands of independent loans, the market became increasingly dependent on a single economic condition: continuously rising home prices.

That assumption was embedded not only in mortgage contracts but also in the models used to value mortgage-backed securities. Historical data suggested that nationwide declines in housing prices were unlikely and that mortgage defaults would remain only weakly correlated. Those assumptions had been reasonable for traditional fixed-rate mortgages. They proved far less reliable for the new generation of refinancing-dependent loans.

Incentives Reinforced the Problem

Securitization also changed incentives throughout the mortgage market.

Originators were rewarded for producing loans rather than holding them. Rating agencies evaluated increasingly complex securities using historical relationships that understated the risks posed by new mortgage products. Investors relied heavily on credit ratings that appeared to transform risky mortgages into exceptionally safe investments.

No single participant needed to behave irrationally for the system to become unstable. Each responded to the incentives before them. The problem was that everyone relied on the same underlying assumption—that refinancing would remain readily available because housing prices would continue to rise.

When Correlation Replaced Diversification

Once housing prices stopped appreciating, refinancing opportunities disappeared. Adjustable-rate mortgages reset. Borrowers who had depended on refinancing suddenly faced payments they could not afford.

Defaults no longer occurred independently. They became highly correlated.

This distinction proved decisive. Securities designed to withstand scattered defaults were not designed to withstand thousands of borrowers encountering the same problem simultaneously. As correlations increased, the diversification that justified high credit ratings largely disappeared.

The weakness was not hidden in the mathematics. It lay in the assumptions behind the mathematics.

From Housing Market to Global Crisis

Securitization connected mortgage markets to virtually every corner of the global financial system. Banks, insurance companies, pension funds, and sovereign wealth funds all held securities backed directly or indirectly by U.S. residential mortgages.

When those securities began losing value, uncertainty spread even faster than losses. Investors could no longer determine which institutions were exposed or by how much. Liquidity evaporated as confidence disappeared, transforming a housing downturn into a full-scale financial crisis.

The lesson is straightforward but profound. Securitization did not fail because financial engineering is inherently flawed. Pooling and distributing risk remain powerful ideas. The failure occurred because the underlying mortgages shared the same structural weakness, and securitization transmitted that weakness throughout the financial system.

When many assets depend on the same fragile assumption, diversification becomes an illusion. A system designed to absorb isolated shocks instead becomes vulnerable to a common one. Mortgage securitization failed in the 2008 financial crisis.

That insight remains as relevant today as it was in 2008. Financial innovation can make markets more resilient, but only when the assumptions embedded in financial products reflect the realities of the assets they are built upon.

Use these insights

Keep your portfolio safe and supercharge your future book by using UFA’s ForeScores to identify profit and manage risk in all types of housing environments and financial conditions.