Every mortgage investor faces the same question: Two borrowers have identical credit scores. Which loan is safer?

Answering that question well means looking at ForeScore, credit score, and mortgage risk together, rather than treating credit history as the whole story

Conventional mortgage valuation has no satisfactory answer. A credit score summarizes a borrower’s financial history, but it says remarkably little about the economic environment in which that borrower must repay a mortgage. It cannot tell whether local employment is strengthening or weakening, whether housing markets are becoming more resilient or more fragile, or whether neighborhood conditions make mortgage distress more—or less—likely.

That omission matters because mortgages do not default in isolation. They default in places where people work, buy homes, experience recessions, and confront unexpected economic shocks.

ForeScore was developed to measure those missing dimensions.

The question, therefore, is not whether ForeScore predicts mortgage performance. It does. The more important question is whether it captures information that the credit score does not already contain.

The answer appears in the data.

Looking at Mortgage Risk in Two Dimensions

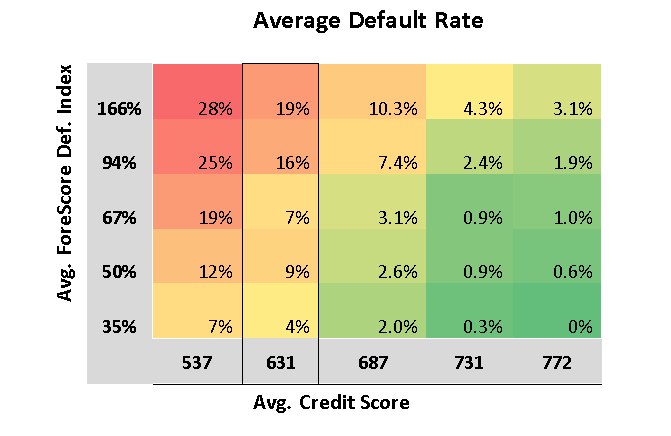

To examine the relationship between borrower credit quality and local economic conditions, we grouped a random sample of 12,500 mortgage originations into twenty-five categories based on two variables: average credit score and ForeScore. We then observed mortgage performance over the following seven years.

The resulting pattern is remarkably clear.

Table 1 reveals an almost textbook example of complementary information. Read down any column and borrowers with similar credit scores experience dramatically different default rates as ForeScore changes. Read across any row and higher credit scores consistently reduce defaults within every ForeScore category.

Neither variable subsumes the other. Each explains variation that the other leaves unexplained.

Table 1. Average realized default rates by credit score and ForeScore quintiles

This table illustrates how credit scores and ForeScore jointly separate mortgage loans into well-defined risk categories. Rows compare borrowers with similar ForeScores across different credit scores. Columns compare borrowers with similar credit scores across different ForeScores. The data are based on a random sample of 12,500 mortgage originations with realized defaults observed over the subsequent seven years.

The table is worth studying carefully because it illustrates a simple but powerful idea: mortgage risk has two dimensions. One reflects the borrower’s financial history. The other reflects the economic resilience of the place where that borrower lives.

Ignoring either dimension leaves important information on the table.

Borrowers with the Same Credit Score Are Not Equally Risky

The clearest illustration comes from borrowers whose average credit score is 631.

Traditional valuation treats these borrowers as broadly comparable. Yet their realized default rates range from only 4 percent in the strongest ForeScore locations to 19 percent in the weakest—a nearly five-fold difference.

Their credit histories are essentially the same.

Their local economies are not.

Those differences cannot be explained by credit scores because the credit scores are already held constant. They arise from local economic conditions that influence whether households can continue making mortgage payments when adversity strikes.

Strong labor markets, resilient housing demand, and stable neighborhoods provide borrowers with more opportunities to avoid default. Weak local economies do the opposite. ForeScore measures those forward-looking conditions.

This is precisely what one hopes to see from a complementary risk measure. If two variables always rank loans identically, one adds little value. But when one meaningfully reorders loans that the other treats as equivalent, it contributes genuinely new information.

ForeScore does exactly that.

Credit Scores Still Matter

The relationship also works in the opposite direction.

Holding ForeScore constant, mortgage defaults decline steadily as credit scores improve. Even within the highest-risk ForeScore group, realized defaults fall from 28 percent among the weakest-credit borrowers to only 3 percent among borrowers with the strongest credit histories.

Credit quality remains one of the most powerful predictors of mortgage performance ever developed.

ForeScore does not replace the credit score. It complements it.

The two measures capture different dimensions of mortgage risk. Credit scores summarize the borrower’s demonstrated willingness and ability to repay based on past behavior. ForeScore summarizes the economic environment in which that repayment must occur.

Together they produce a more complete assessment than either can alone.

The Most Interesting Result Is Their Interaction

The most important insight does not come from any single row or column.

It comes from how the two measures interact. Across all credit score tiers defaults in the ForeScore quintiles increase about five fold.

Borrowers with excellent credit remain relatively resilient across a wide range of local economic environments. Changes in ForeScore certainly matter, although the relative differences is about five fold, the absolute differences are modest, from near zero to 3-4%.

Borrowers with weaker credit tell a different story. For these loans, the same change in local economic conditions can also increase observed default rates by a factor of five. But now the absolute difference in the second credit decile is from 4% to 19%, an increase of 15%!

This is a classic interaction effect. Credit quality influences how sensitive borrowers are to local economic conditions, while local economic conditions influence how much credit quality ultimately matters.

As borrower quality declines, location becomes increasingly important.

That is precisely where valuation decisions become most difficult—and where additional information becomes most valuable.

The implications extend beyond default probabilities. Expected losses are substantially larger among lower-credit borrowers, making loan values increasingly sensitive to local economic conditions. Two mortgages with similar credit scores can therefore have materially different economic values simply because they are originated in different markets.

Investors who ignore location risk inevitably miss these differences.

Why This Matters

These findings have practical implications for every stage of mortgage investing.

When investors rely exclusively on credit scores, they inevitably group together loans whose realized risks differ substantially. The result is systematic mispricing. Safer loans subsidize riskier ones. Loss reserves become less accurate. Capital is allocated less efficiently. Creditworthy borrowers may even be declined because they belong to broad credit categories that conceal important differences.

Adding ForeScore improves risk segmentation by distinguishing borrowers who appear identical through the narrow lens of credit history but face very different economic futures.

Better segmentation leads directly to better pricing, more accurate reserve estimates, stronger portfolio surveillance, and more disciplined risk management.

Perhaps most important, it allows investors to identify profitable lending opportunities that conventional models overlook while avoiding risks that traditional credit measures underestimate.

Finance advances by measuring risk more accurately.

Credit scores represented one of the great innovations in consumer finance because they transformed millions of individual borrowing histories into reliable forecasts of repayment.

ForeScore extends that same logic.

Rather than replacing the credit score, it measures something the credit score was never designed to capture: the economic resilience of the places where mortgages are repaid.

The evidence suggests that both signals matter.

Together they provide a substantially more complete picture of mortgage risk than either can provide alone.

See the Evidence in Your Own Portfolio

UFA’s ForeScore Risk Analysis segments mortgage portfolios simultaneously by borrower credit quality and local economic conditions, providing forward-looking forecasts of default and prepayment risk for pricing, portfolio surveillance, reserve estimation, and investment analysis.

The twenty-five borrower segments shown in this article can be replicated using your own portfolio, allowing investors to see exactly where location risk adds information beyond traditional credit scores.

Request a ForeScore Risk Analysis report to see how your portfolio is distributed across these risk categories—and where additional insight can improve investment decisions.