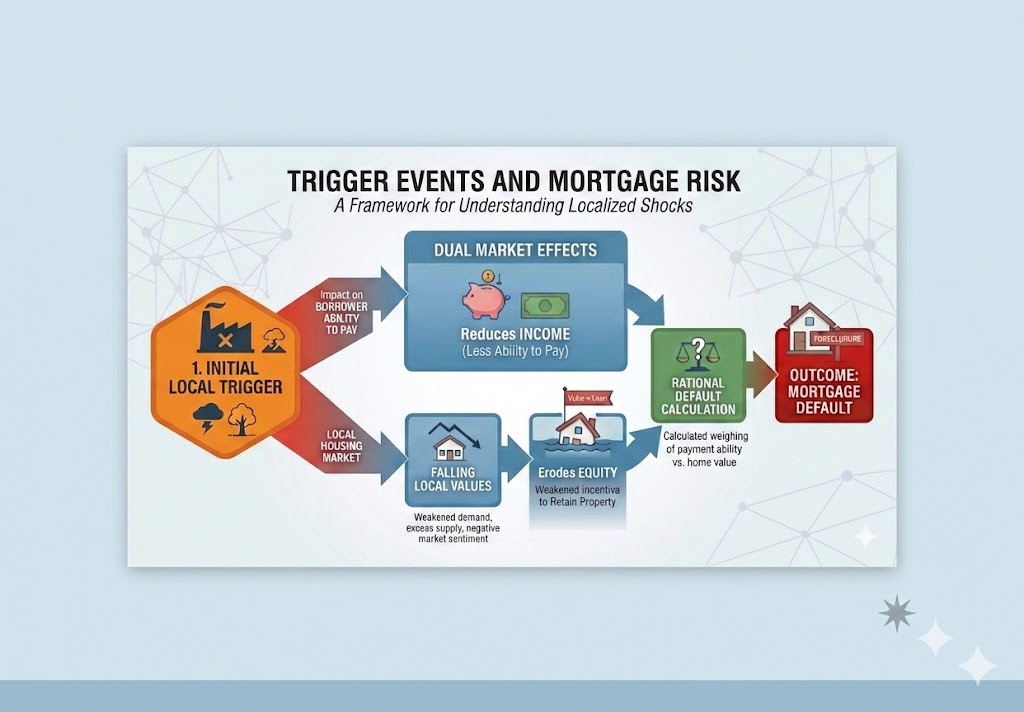

Mortgage default is often described as a financial decision—an optimization problem where borrowers weigh the costs and benefits of continuing to pay. Capozza et al. remind us that this framing is incomplete. Default is also a household economic shock story, and those shocks are overwhelmingly local — local economic shocks trigger mortgage default.

Borrowers don’t lose their jobs “nationally.” They lose them because a factory closes, a hospital downsizes, or a local employer relocates. They don’t experience income volatility in the abstract. They experience it because their industry is cyclical, their hours are cut, or their region is exposed to a narrow employment base. These local shocks shape the borrower’s ability to pay—and they vary dramatically across markets.

Local Labor Markets Drive Default Risk

The research shows that local unemployment spikes are far more predictive of default than national unemployment rates. A national recession might raise unemployment by 1–2 percentage points, but a local plant closure can raise unemployment by 10–15 points in a single county.

This asymmetry explains why:

- Some metros experience default waves even when national conditions look stable

- Borrowers with identical credit profiles behave differently depending on where they live

- National models consistently underestimate risk in vulnerable local markets

Local labor markets are not just noisier versions of national trends—they are structurally different, shaped by industry concentration, occupational mix, and regional economic resilience.

Income Volatility: The Hidden Local Risk Factor

Income volatility is another local variable that national models fail to capture. Markets dominated by:

- Tourism

- Construction

- Manufacturing

- Energy extraction

- Seasonal industries

experience sharper swings in household income. These swings translate directly into higher delinquency and default rates, especially for borrowers with thin financial buffers.

Income instability amplifies the effect of price declines, creating a double‑shock environment where borrowers face both falling equity and falling earnings.

Migration: The Slow‑Burn Shock That Weakens Housing Markets

Equally important is migration: Migration flows—both in‑migration and out‑migration—play a critical role in shaping local housing demand. Consequently, When households leave a region:

- Demand softens

- Inventory rises

- Prices weaken

- Liquidity dries up

This creates a feedback loop: weaker demand depresses prices, which increases negative equity, which raises default risk for those who remain.

Conversely, strong in‑migration can stabilize markets even during national downturns by supporting prices and maintaining liquidity.

Migration is one of the clearest examples of why local markets diverge sharply, even within the same state or metro area.

Local Shocks Interact With Local Price Cycles

The most powerful insight is that local economic shocks and local price cycles reinforce each other:

- A job loss is more likely to lead to default when the borrower is underwater

- A price decline is more likely to push borrowers underwater when income volatility is high

- Out‑migration accelerates price declines, which accelerates negative equity, which accelerates default

This interaction is why default risk is nonlinear and spatially clustered. It’s not one shock that triggers default—it’s the combination of local shocks hitting local price cycles.

Why This Matters for Modern Mortgage Analytics

Understanding local economic shocks is essential for:

- PD modeling: Local unemployment and income volatility must be embedded directly into risk models

- Stress testing: Scenarios must include geographically heterogeneous labor‑market shocks

- Surveillance: Early‑warning systems must track local job growth, wage trends, and migration patterns

- Credit policy: Lenders must adjust guidelines based on local economic resilience

Ignoring local shocks leads to systematic underestimation of risk—especially in markets with concentrated employment bases or volatile income structures. Local economic shocks trigger mortgage default.

Future reading

In a future post, we’ll explore how borrower characteristics interact with local conditions, and why identical borrowers can have radically different default probabilities depending on the economic environment around them.

Use these insights

Keep your current loans safe and supercharge your future lending portfolio by using our ForeScores to identify profit and manage risk in local housing environments.